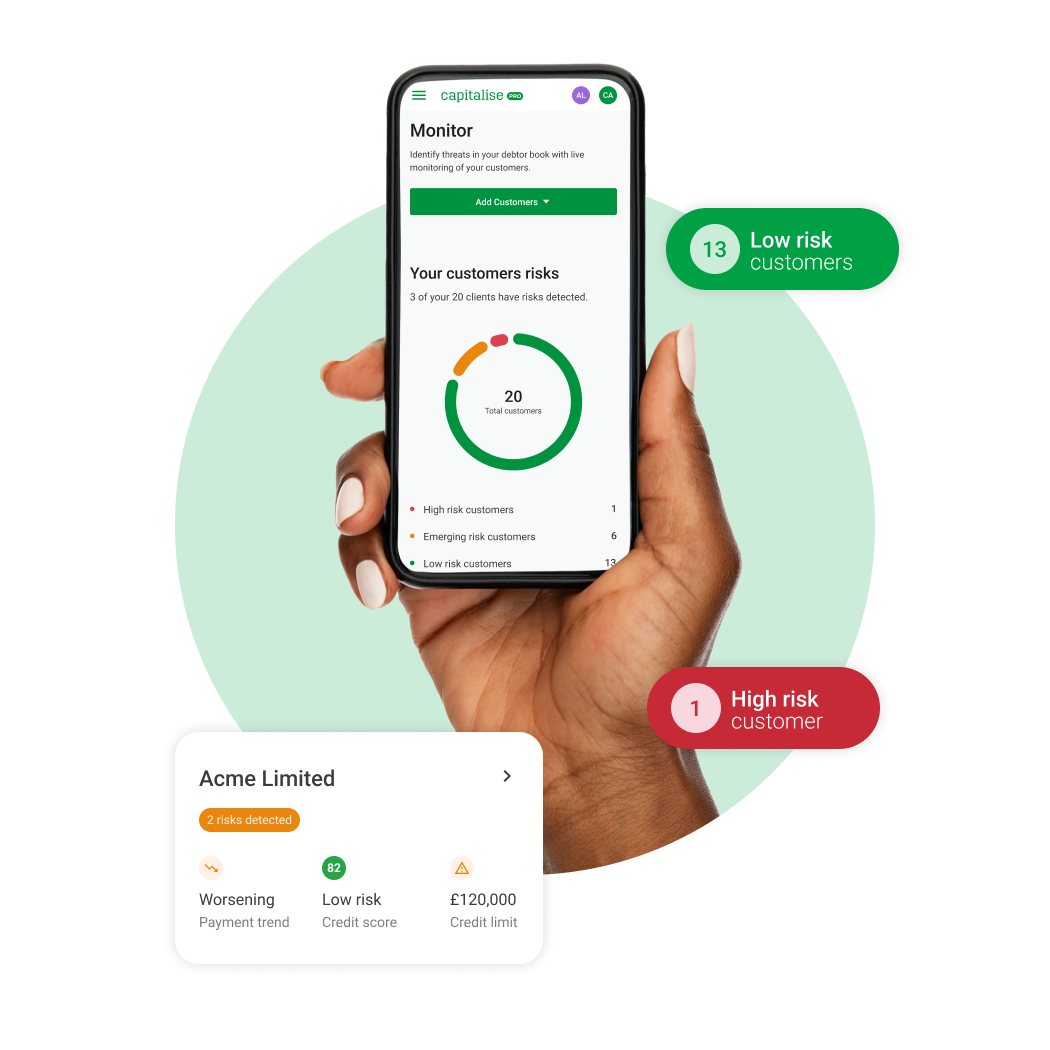

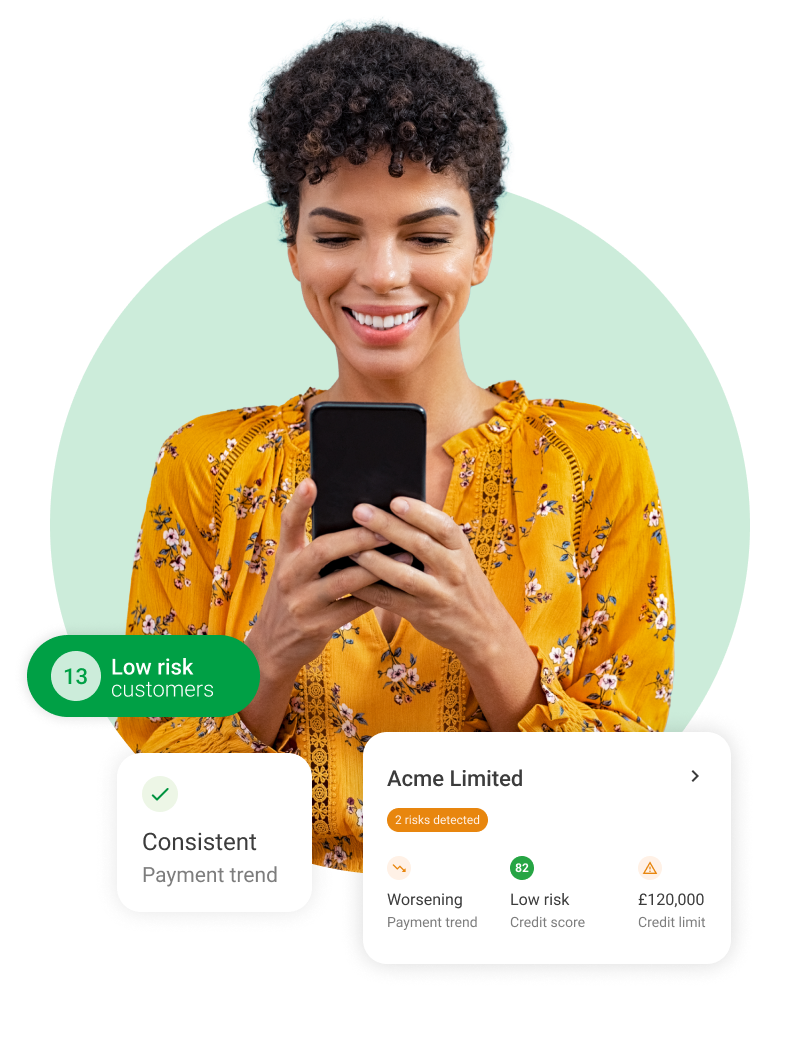

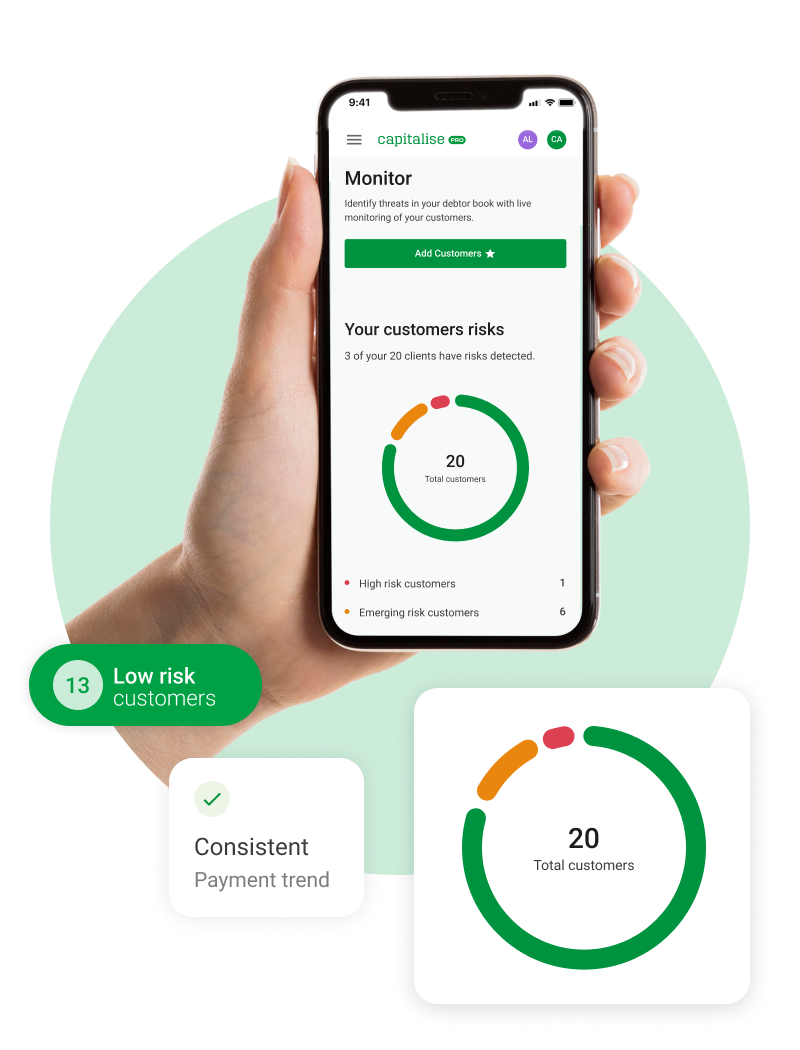

Full credit profile - as lenders see it

Your full business credit score

Improve your credit score. Get better funding. Reduce risk to your business.

All when you upgrade to Capitalise for Business Pro from £19/month

Compare features

Our instant business credit reports are powered by Experian.