A commercial mortgage offers lower interest rates than unsecured loans and flexible repayment terms of up to 25 years, making it a smart financing option to grow your business

A commercial mortgage is a loan used to buy or refinance a property for business purposes, such as an office building, a shop, or a warehouse. Unlike a residential mortgage, which is for personal homes, a commercial mortgage is only used for properties that generate income or support a business.

A commercial mortgage cannot be taken out on the borrower’s principal primary residence.

With a commercial mortgage, the property itself is typically used as collateral. Loan terms, interest rates, and repayment schedules vary based on factors such as the loan amount, property type, and the borrower's financial profile.

Commercial mortgages can be used to both purchase a business property or to raise capital by refinancing a premises you own.

They are taken out over a pre-determined number of years with any charges, interest rates and fees transparently outlined upfront so you'll be able to budget effectively.

A commercial mortgage can come either with a variable interest rate, or a fixed interest rate.

With access to a whole marketplace of lenders, you can compare multiple offers to find the best terms for your business.

You can spread the cost of your loan over a longer period - often up to 25 years - for more affordable monthly repayments and to help you manage cash flow effectively.

Commercial mortgages generally offer lower interest rates than unsecured loans because the property serves as collateral. While rates may be higher than residential mortgages, they’re a competitive option for business owners.

You’ll get support from one of our dedicated funding specialists who have experience supporting businesses in secured complex property finance deals. They’ll be on hand to guide you throughout the process.

| Advantages | Disadvantages |

|---|---|

| Lower interest rates compared to unsecured loans | Usually requires a larger deposit (at least 25%) than residential mortgage |

| Long term repayment options (up to 25 years) | Property must be used for commercial purposes |

| Can help with property purchases or refinancing | Interest rates may be higher than residential mortgages |

| Flexibility in property usage (business premises, investment, etc. | May involve upfront fees and charges, such as an arrangement fee |

This is a fee charged by the lender for processing and setting up your mortgage. It usually gets added to the total amount of your loan. The arrangement fee is typically around 1% of the loan amount, though this can vary depending on the lender. It covers the work the lender does to arrange your mortgage.

This fee covers the cost of a professional property valuation. Typically, you'll pay the fee to the lender, who will arrange the valuation. It must be paid before you can proceed with your loan application. The valuation helps the lender confirm the property's value, giving them confidence in lending against it.

These fees cover the legal work needed to complete the mortgage. This could include property searches, transferring ownership, and other legal tasks. While these fees are separate from the mortgage itself, they are necessary to finalise the property purchase and legally transfer it into yours or your business’ name.

Interest is the cost you pay for borrowing the money. This will be charged over the life of the loan and can vary based on your interest rate. The higher the interest rate, the more you’ll pay over time. The interest rate is often influenced by factors like your creditworthiness, the deposit amount and the Band of England base rate.

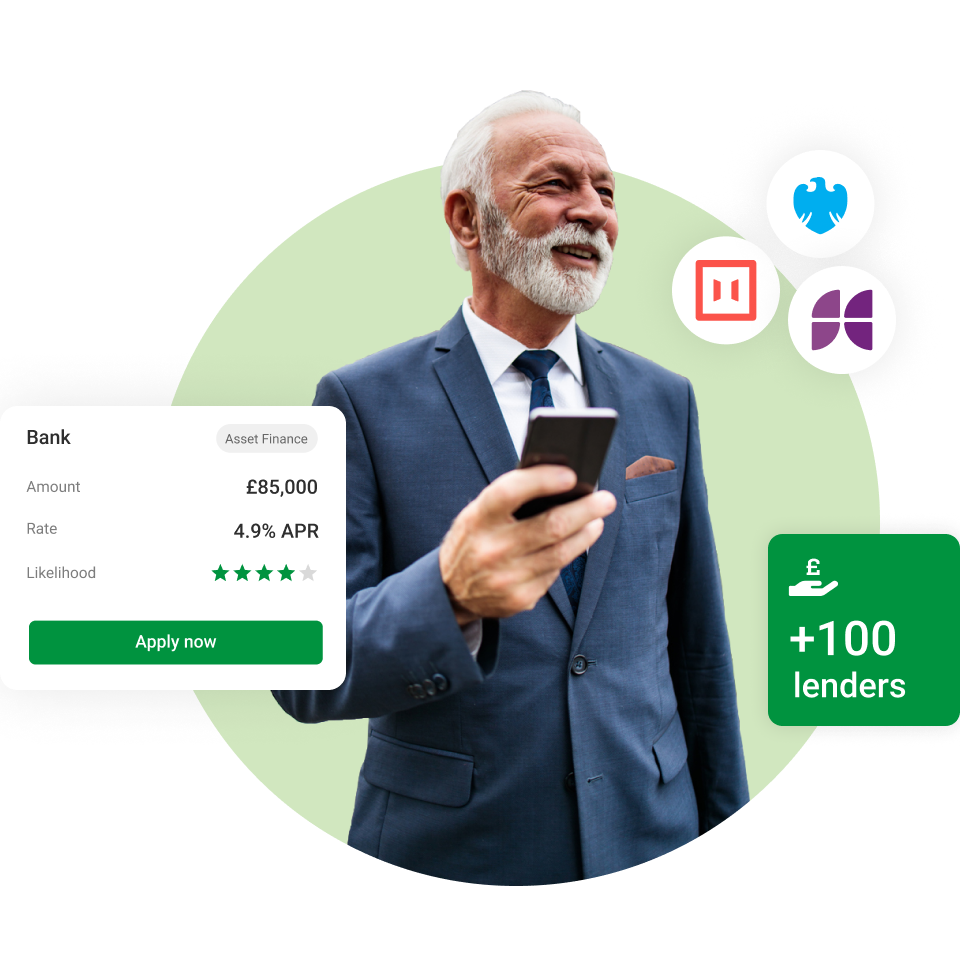

Capitalise is an FCA regulated platform dedicated to UK businesses. Our mission is to help businesses to take control of their financial health. We support business owners by providing easy way to access over 100 lenders and compare their loan products. Our advanced platform makes intelligent matches and ranks lenders, based on their past successes, to help businesses select the best funding solution.

Capitalise also enables businesses to check their own Experian business credit score to better understand their financial health. Plus businesses can check the credit profiles of the companies they work with to reduce risk.

Yes, you can get a commercial mortgage if you're looking to purchase or refinance a property for your business.

Yes, in most cases, the interest on commercial mortgages can be tax-deductible as a business expense. However, you should consult a tax advisor to understand the specifics for your individual circumstances.

Typically, you'll need a deposit of at least 25% of the property's value. The exact amount will depend on the lender and the type of property you're buying.

Yes, commercial mortgage rates are generally higher than residential mortgage rates, as commercial properties are considered riskier investments. However, commercial mortgages do usually have lower interest rates than unsecured business loans, so can still be a competitive option for your business

There are a few key differentiators between commercial mortgages and personal mortgages, the obvious being that commercial mortgages are for business purposes, and personal mortgages are for the buyer to live in.

The key differences you’ll need to know as a potential buyer are:

Yes, it's possible to get a commercial mortgage through a limited company and it may even come with tax benefits.

A lender will assess the affordability of the mortgage based on the strength of the applying business, so it’s worth bearing in mind that the business should be able to show clear affordability for the monthly mortgage repayments.

No, you don’t need to set up a limited company to get a commercial mortgage. Many sole traders also explore this type of loan. Just get in touch with us, and one of our funding specialists will help you understand how much you can borrow and whether you're eligible for a commercial mortgage based on your individual circumstances.

United Kingdom

United Kingdom  South Africa

South Africa