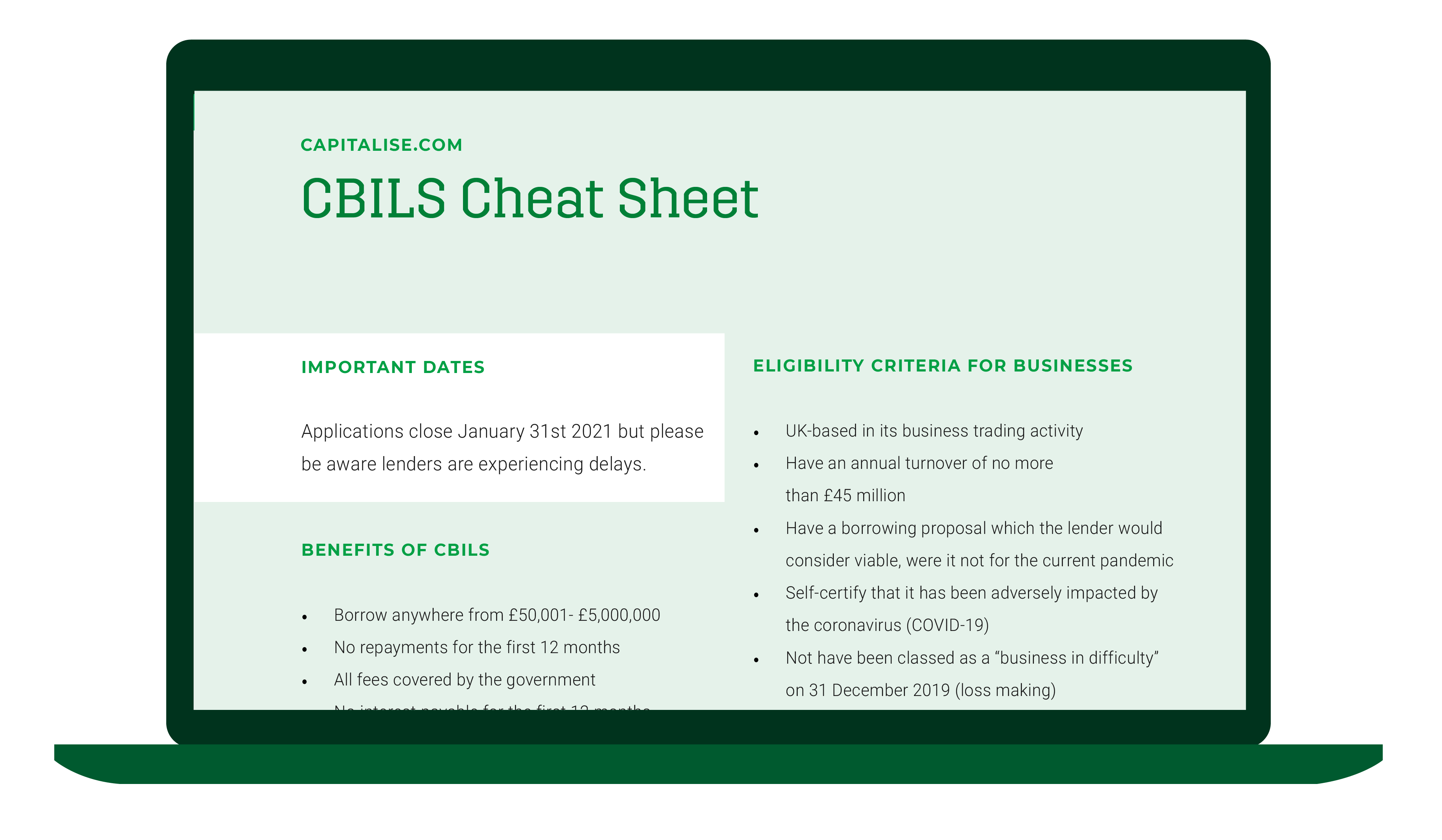

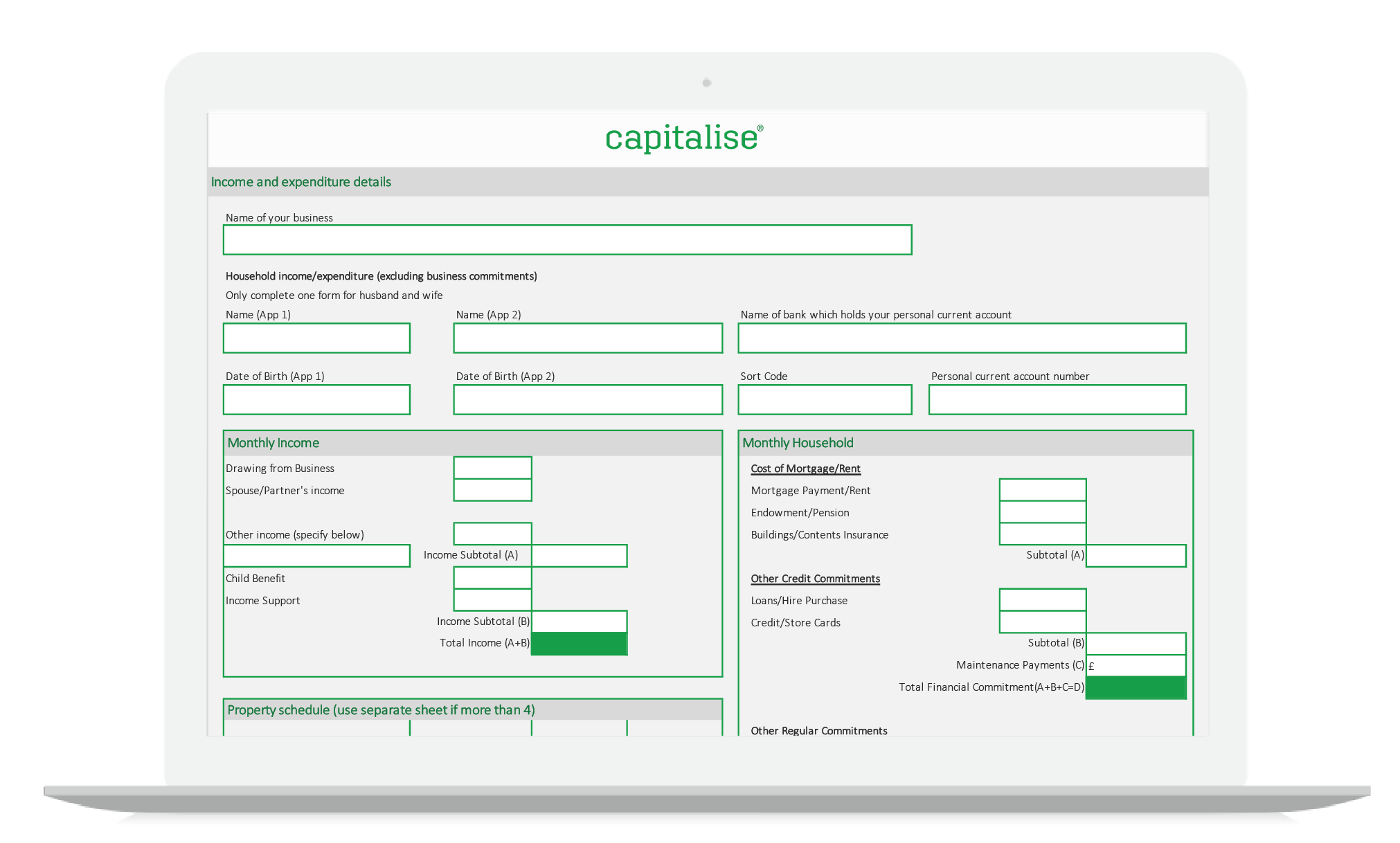

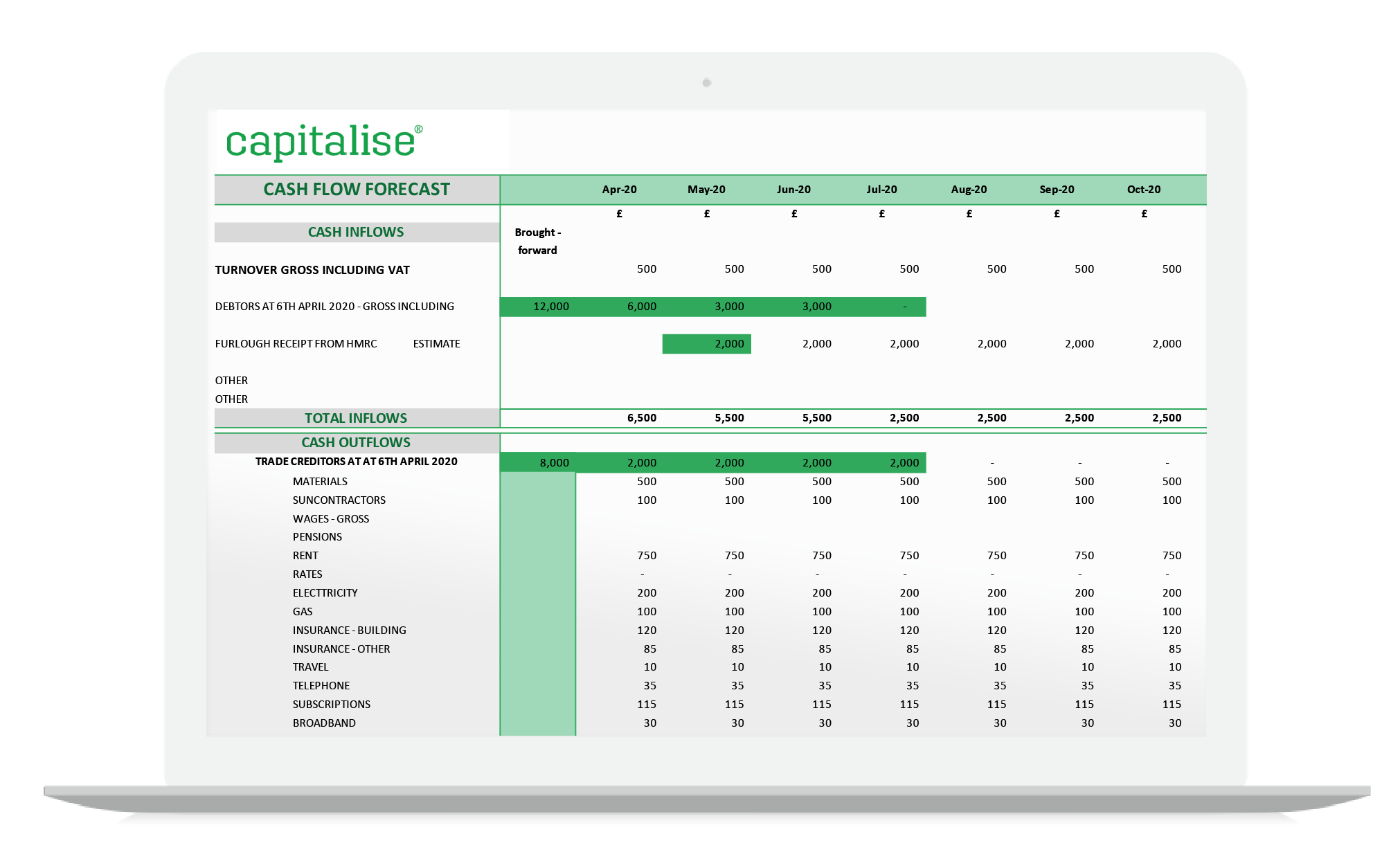

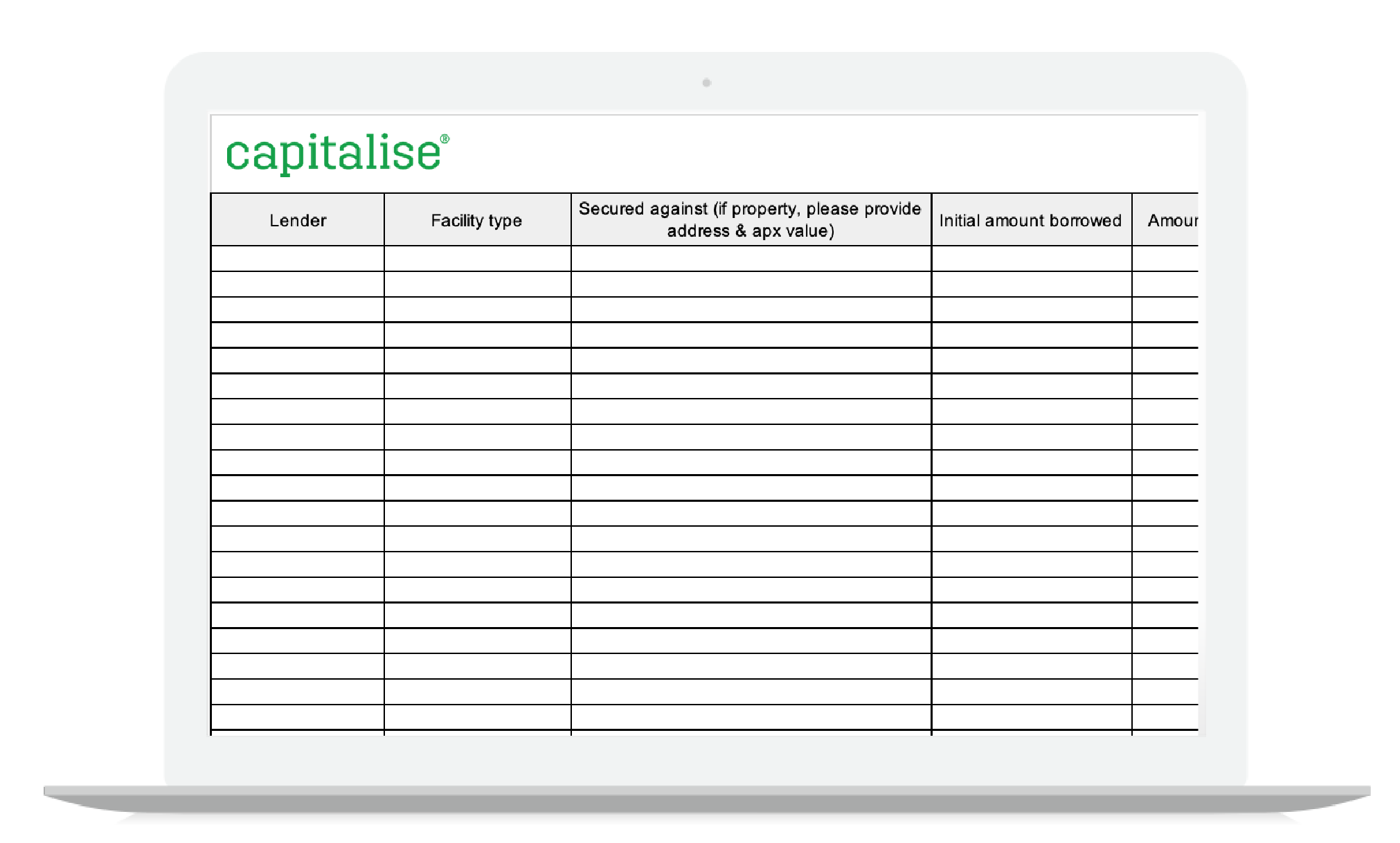

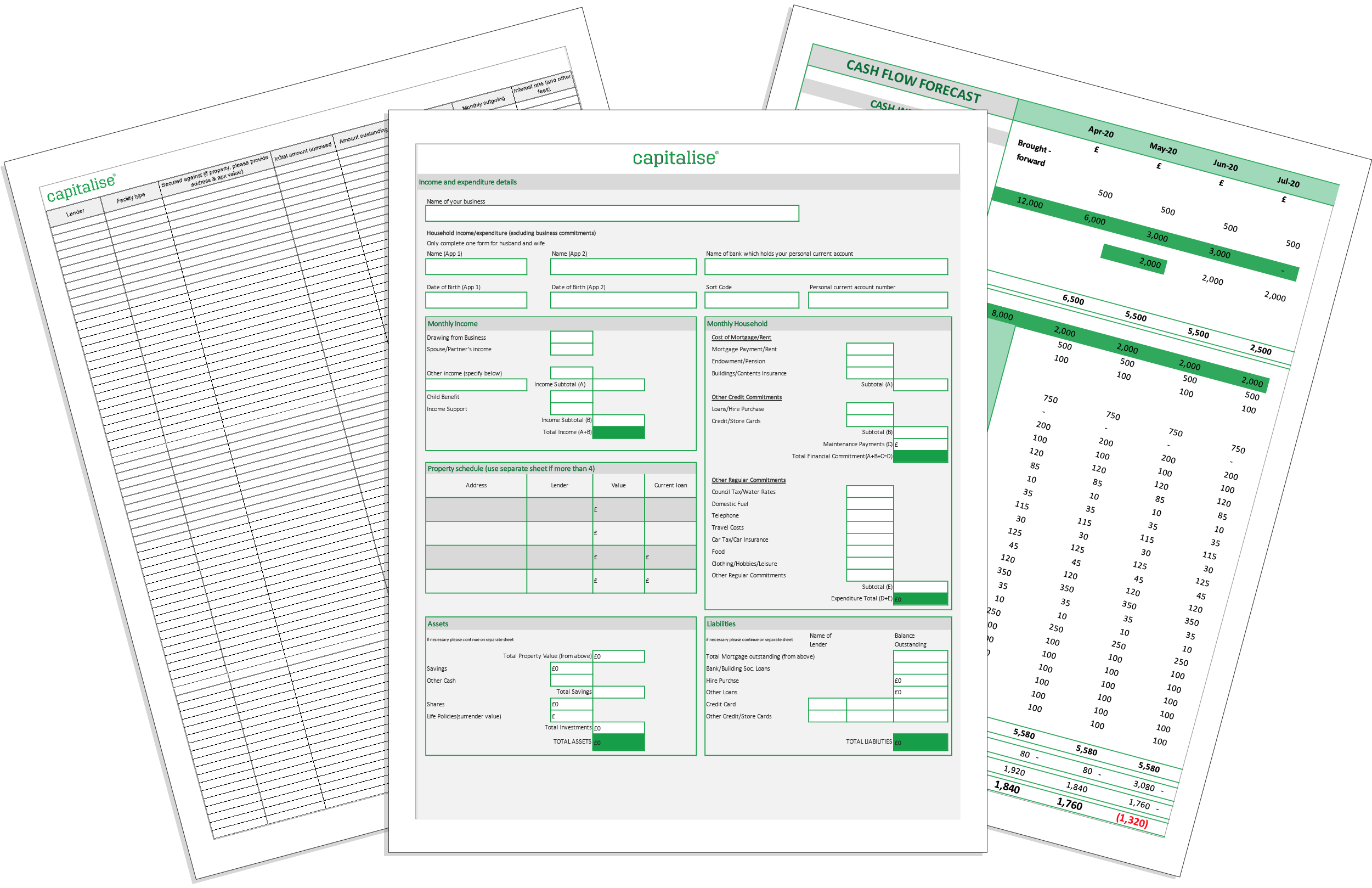

Coronavirus Business Interruption Loan Scheme (CBILS) process is new to us all. These templates will make it easier for you complete applications and give lenders a good insight into the affordability of your clients.

CBILS is a programme run by the British Business Bank to support businesses who can afford lending products but lack the security necessary to be approved.

Whilst we're all learning the process as we go along, we are sharing the templates that will make it easier for you complete CBILS applications